House Prices Surge to Record High due to “Mini Boom”

Following the reopening of the housing market and the Scottish Government’s announcement that they were increasing the nil rate band for Land and Buildings Transaction TAX (“LBTT”) from £145,000 to £250,000 there has been more good news for the housing market.

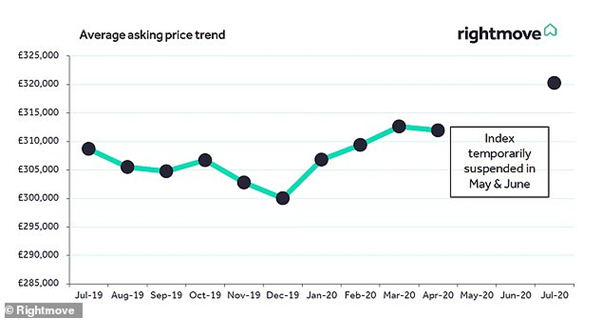

According to Rightmove the average price of properties coming to the market across the UK is 2.4% higher than before lockdown started in March. Figures released by Rightmove indicate that the average property price in Scotland is £166,322 which is a 4.5% increase since March. This was the highest percentage increase across the UK.

Miles Shipside, a Director at Rightmove, commented that “the unexpected mini-boom continues to gather momentum.”

With the change in LBTT lasting until 31st March 2021 and buyers reassessing their housing needs and lifestyles it will be interesting to see how this develops.

Our award winning Estate Agents in Paisley and Renfrew have seen a surge in enquiries since the market reopened. If you are looking to sell a property get in contact today to arrange your Free Valuation and a member of our experienced team will be in touch. In addition, our conveyancing solicitors in Paisley and Renfrew are on hand to provide you with all the necessary legal advice when it comes to buying and selling a property.

Covid-19 - Moving Home in Scotland to be Allowed from 29th June 2020

On Thursday 18th June 2020, Nicola Sturgeon unveiled plans for Scotland to move into Phase 2 of the Scottish Government’s Route Map aimed at easing lockdown restrictions. Restrictions on moving home are to be lifted from Monday 29th June 2020. The detailed guidance on the Scottish Government’s website states:-

“During phase 2, members of the public will be allowed to leave their homes in order to undertake certain activities in connection with the purchase, sale, letting or rental of a residential property which are expected to include:

- visiting estate or letting agents, developer sales offices or show homes;

- viewing residential properties to look for a property to buy or rent;

- preparing a residential property to move in;

- moving home; or

- visiting a residential property to undertake any activities required for the rental or sale of that property.

This will allow people working for relevant organisations and businesses to travel to work where necessary in order to undertake these activities in a safe manner. A key change is that a home move will no longer have to be reasonably necessary; home moves will be permitted. Everyone should still comply with the physical distancing and health guidelines”.

If your plans to move home have been affected by the lockdown restrictions, if you are just starting to think about moving home or even if you are a first time buyer get in touch with our experienced conveyancing solicitors in Paisley and we will guide you through the process.

The Effect of the Covid-19 Outbreak on Property Sales and Purchases in Scotland

Moving home is usually the biggest transaction anyone will undertake. The potential impact of the Covid-19 outbreak will be a real concern for anyone involved in buying or selling property in Scotland right now. We have been working hard to keep our lines of communication open with our clients and other solicitors to ensure that everyone is kept up to date on the latest developments from The Scottish Government, The Law Society of Scotland, the Registers of Scotland and we can work towards completion of these transactions as soon as it is safe to do so.

The Registers of Scotland closed for business on 24th March which effectively brought all property transactions to a pause. Since then, the Law Society has worked together with lenders and the Registers of Scotland to bring in interim measures to allow some essential transactions to proceed. The Government has also issued separate advice to everyone moving home at this time, which can be found here: https://www.gov.scot/publications/coronavirus-covid-19-guidance-moving-home/.

Advice For Homeowners

Essentially, the advice to everyone is to stay at home and delay transactions where at all possible. It is our experience that our clients wish to adhere to this policy and all parties have amicably agreed to pause proceedings and agree a future date of entry when the restrictions are lifted. During this lockdown period we will still be available to discuss matters with you and we will use this time to carry out the necessary conveyancing with the solicitors on the other side of the transaction so that when the restrictions are lifted, we can look to agree new dates of entry and complete your transaction as soon as possible.

We are aware that there have been conflicting reports as to whether transactions can still proceed at this time and a small number of transactions may have completed during the lockdown period. We would highlight that the advice from the Scottish Government is that all transactions should be postponed, even where there is a concluded contract. In order to proceed during the lockdown period, the move would need to be reasonably necessary in accordance with your circumstances and those of the other parties involved. In addition, you would require to show that you would be in a position to move safely, without involving removal companies or third parties and the property into which you are moving to would require to be empty or safely vacated. Even where these criteria are met, it may be that the solicitor on the other side of a transaction, or somewhere further down the chain, is not in a position to complete and therefore the transaction could not complete at this time.

Registers of Scotland - Online Portal Clarification

The Registers of Scotland opened a digital portal on 27th April and this has made news headlines, leading many to think that house moves can proceed as normal again. Unfortunately, this is not currently the case due to the Scottish Government’s lockdown restrictions, which are not to be reviewed again until 7th May 2020. The digital portal opened by the Registers of Scotland is not a full re-opening of the Application Record and they are currently only accepting a small number of applications based on transactions which were due to complete at the end of February at the moment. They will move this date forward only when they have completed the applications received through the digital portal at this time. It is vital that when we complete your transaction we are able to send your application to the Registers of Scotland immediately after completion, for the protection of both you and your lender.

We understand this is a worrying time for all our clients, and the situation is complex, so please do not hesitate to contact Kathryn Gibb in our property department to discuss your particular circumstances. Kathryn can be contacted by calling 0141 887 5271 or by completing our online enquiry form.

Registers of Scotland: Latest House Price Index Report

The latest monthly House Price Index Report for Scotland has been published by the Registers of Scotland. This month's edition gives us the average price of residential property across Scotland for August 2017 and the volume of sales for June 2017 (the latest dates for which these data are available).

The latest monthly House Price Index Report for Scotland has been published by the Registers of Scotland. This month's edition gives us the average price of residential property across Scotland for August 2017 and the volume of sales for June 2017 (the latest dates for which these data are available).

The Report shows an increase in the average price of residential property in Scotland now stands at £146,354. This is an increase of 3.9% against the August 2017 figure.

It's good news too for the number of residential properties sold. In June 2017, there were 10,473 sales in the month. That's an increase of 9.3% over the June 2016 figure. It’s also a 26.2% increase over the May 2017 figure.

Scottish House Price Changes

The City of Glasgow local authority area saw an increase of 5.7% in the average price, rising to £125,634 in August and led the sales volume chart with 1,224 sales in June - an increase of 20.6% over the June 2016 figure.

In Renfrewshire, the average price of a property was £122,549 in August 2017. That’s an increase of 6.5% against the same month in 2016. In terms of the number of properties sold, the report indicates that in June 2017 there were 409 sales of residential property registered with the Registers of Scotland. This is an increase of 17.5% against the June 2016 figure.

To read this month's Scottish House Price Index Report, click here.

Mortgage Lending up 12% in May

The latest release of date from the Council of Mortgage Lenders (CML) shows that lending in May increased 12% when compared to April’s figure. Standing at £20.1 billion, it is also ahead of the May 2016 figure when it stood at £17.9 billion. However, it’s not all positive growth. The CML has also revised down its forecast for buy-to-let mortgages for 2017 and 2018.In December 2016, it had forecast lending of £38 billion in both 2017 and 2018. These figures have been reduced to £35 billion in 2017 and £33 billion in 2018.

Paul Smee, Director General of CML commented:

“Re-mortgage activity and first-time buyers continue to drive lending this year. Looking ahead, we expect to see this trend continue, but not as strongly, as the factors supporting lending are blunted by less favourable economic conditions.

Buy-to-let had a weak start to 2017, and the sector’s contribution to overall net mortgage lending has fallen considerably over the last year.

While falling mortgage interest rates have helped support borrowing, tax and prudential measures are exerting pressure on the buy-to-let market. Following the distortion of the stamp duty change on second properties last year, we expected a slight recovery in lending levels. However, this has not materialised, and we therefore have lowered our forecast for buy-to-let lending this year and next.

This re-emphasises the case for avoiding further changes to the tax and regulatory framework until the effect of these already in train have been properly assessed.”

Contact Us

If you’re thinking of moving house, contact our experienced estate agents and property solicitors on 0141 887 5271 (Paisley) or 0141 886 5678 (Renfrew).

Thinking about selling? Now’s the time

We have seen a very different, vastly improved property market for sellers this year. Many of our clients have been surprised at just how good a result we’ve managed to achieve for them.

We have seen a very different, vastly improved property market for sellers this year. Many of our clients have been surprised at just how good a result we’ve managed to achieve for them.

It is all about supply and demand. The market is underpinned right now by a good demand amongst buyers, this is certainly helped, amongst other things, by the cheap mortgage lending available. However, this is set against an insufficient supply of new properties being made available for sale. Demand is growing, but the supply is not keeping pace.

Clearly this is good for sellers. This year we have been seeing shorter sale times, frequent closing dates off the back of multiple viewings and, as a result, sometimes surprisingly good sale prices. This is especially true for family size homes. So, if you are thinking about moving, now could be the perfect time.

There is no better example of this than our recent marketing of 13, 15, 18 Kemp Avenue, 11 Methuen Road and 50 Clydesdale Avenue in Paisley. These properties are all within 500 yards of each other and are all of a similar type and value. We brought these properties to the market over the last few weeks, but they are all sold now.

What is striking is that none of the properties were on the market for longer than two weeks. In fact, Number 18 Kemp Avenue lasted only two days. Numbers 13 and 15 Kemp Avenue sold at closing dates with multiple offers above valuation. It goes to show, even with multiple properties coming to market in a concentrated location around the same time, the demand is still there for them to be snapped up.

There are still buyers who missed out on these properties. We are working with them now to help them find another home.

The bottom line is this: we are currently experiencing a high demand for family homes. We have serious buyers actively looking for property. We are confident that they would pay a premium price for the right property.

Contact one of our experienced staff today

So, if you are thinking about selling contact one of our experienced staff today to arrange a free valuation on 0141 886 5678. We are offering competitive fee packages for any newsletter enquiries.

Helping you get on the property ladder without the Bank of Mum and Dad

It appears that the “Bank of Mum and Dad” is becoming an increasingly popular avenue among first time buyers for property funding. Research suggests that the Bank of Mum and Dad will lend over £6.5 billion in 2017 to help their children get on the property ladder, a £1.5 billion increase from last year. As a result, the Bank of Mum and Dad is now the 9th largest mortgage lender in the UK!

So, where has this all stemmed from? A key factor affecting this trend is intergenerational inequality, with young adults subject to limited opportunities in comparison to the baby boomers with regards to affordable housing and defined benefit pensions. Research shows on average, parents will lend around £21,600 this year with Millennials being the biggest recipients with 79% of the funding going to people under 30.

However, statistics suggest that in fact, lending from parents is doing more harm than good, nor is it sustainable or equitable for both parents and the young people. It’s understandable that parents want to help get their children on the property ladder, but it’s also one of the causes of our broken housing market.

At Walker Laird, we offer the opportunity for first time buyers to meet with us and chat through the whole process of home buying, including arranging your mortgage. We can put you in touch with a mortgage advisor who will be able to search the market for the mortgage that best suits your needs. To make things easier, the mortgage advisor will offer to meet you in your own home in the evening if you prefer. It doesn’t end there, we will help you negotiate prices with the estate agents, help you submit your offer and help you seal the deal.

We understand that purchasing your first home is costly enough. This is why our initial advice is free of charge and you’ll only pay a fee if your offer is accepted as we start to deal with the conveyancing process.

Sound good?

Further Information

Please get in touch for more information Paisley: 0141 887 5271 and Renfrew: 0141 886 5678.

Helping your children get on the property ladder

The bank of mum and dad is a cliché that’s well worked in today’s economic times, not least when it comes to helping children to get a leg up onto the property ladder. Rising property prices and lenders restricting the level of borrowing has meant that younger people have found it increasingly difficult to bridge the gap between the amount they are able to borrow and the price they have to pay for the property.

Many parents and grandparents who have the financial wherewithal to help need to consider very carefully how to go about providing any sort of assistance to their children or grandchildren.

The option of helping with the deposit without any expectation of this being repaid is straightforward – it’s a simple gift from one to the other.

However, if the plan is to provide a home for the child, then there are potential difficulties that need to be addressed before embarking on such a scheme.

If the title to the property is to be taken in the name of the child, then the child can subsequently do what he or she wants with that property. The child can borrow money and use the property as security or sell the property and keep the proceeds of that sale.

If the child were to run into financial trouble and be pursued by creditors to the point he or she becomes bankrupt, that is likely to lead to the property being sold to meet the debts the child has run up.

Should the child be married and the marriage fail, it is likely that there will be a claim by the spouse for a share in the value of the property.

You should also be aware that if the child is under the age of 16, even though they take the title in their own name, the purchase will be considered as a purchase of an additional dwelling and the rules relating to the Additional Dwelling Supplement will apply. The Additional Dwelling Supplement is a tax of 3% of the purchase price of the property (if the property is purchased for more than £40,000) that is charged when someone buys a property in addition to their current main residence - and is payable in addition to any Land & Buildings Transaction Tax (in England and Wales, Stamp Duty) that may already apply.

Parents and grandparents must think through the options very carefully before embarking on any such scheme.

So, what are the options to secure the position for the parents and grandparents?

There is always the option of buying the property either with or without a loan and then allowing the child to live in it. This would mean that the property would always belong to the parents or grandparents and when it is eventually disposed of, it is likely that Capital Gains Tax will need to be paid on any gain achieved on that sale. If the parents or grandparents already own their own home, there is also the added cost of the Additional Dwelling Supplement.

If the parent holding title to the property were to die, then the property will form part of the estate – and there may be other siblings who are entitled to share in the estate and that might mean that the property must be sold to satisfy that entitlement. Even this method of helping has its problems!

As an option, to try to at least secure the money invested in the property, the parent or grandparent might decide to secure their interest by taking a Standard Security over the property. If this is done, it’s usually backed up by an Agreement setting out in what circumstances any money secured should be repaid. That’s fine as far as it goes because even if there is a problem and the property has to be disposed of, then the money paid to buy it (and potentially any notional interest payable on that money as might be provided for in an agreement) would need to be repaid – but the parent or grandparent might not be able to share in any profit on the sale. If the property is in the child’s name, then the same problems can arise regarding bankruptcy or divorce as mentioned above, but of course, the security would go some way to protect the money invested!

One option that has been getting more attention in recent times is the creation of a trust. The basic methodology is that a trust is created with the parents or grandparents as trustees and the child as a beneficiary. The property is then purchased by the trust with money put into the trust by the parents and/or grandparents. The trust then becomes the owner of the property. The child can live in the property and be sheltered from the vagaries of divorce, separation or bankruptcy as none of these events could have an effect on the ownership of the property – it’s owned by the trust!

The trust can sell the property and buy another property and allow the child to live in it and it can ultimately transfer the property to the child or dispose of it and pass the free proceeds of that sale to the child.

There are also taxation implications that will need to be addressed. The Additional Dwelling Supplement we discussed above will apply to a purchase of this nature if the parents or grandparents who created the trust own their own homes. On disposal,

Capital Gains Tax may apply. It is beyond the scope of this article to enter into a detailed discussion of when Capital Gains Tax will apply so for further information on that we would direct you to the Government website dealing with this topic. You can access that by clicking here. One important point to note is that the money paid into the trust to enable the trust to purchase the property, no longer forms part of the parent’s estate and, as such, is sheltered from Inheritance Tax. Again, to ensure that this is done correctly, you need to take proper legal advice on this.

Contact Us

If you find yourself in such a situation or are currently considering your options, we’d be happy to speak to you about this. Please call us on 0141 887 5271 (Paisley) or 0141 886 5678 (Renfrew).

Open house event this weekend

We will be holding an open house weekend for selected properties on Saturday 28th and Sunday 29th January. Please see below for details of the properties taking part.

Open house viewing allows potential buyers the opportunity to view property without the need to contact the Estate Agent to arrange an appointment. Home buying can be a fairly daunting process, particularly for first time and inexperienced buyers. All too often we find that new buyers can be apprehensive to arrange viewing, not knowing what is expected of them. We want to alleviate that fear and encourage the viewers to look at our properties on an informal basis.

If a buyer sees something that they are interested in, then we can provide all the help that they need in order to proceed with the purchase. We also find that buyers tend to look at a broader spectrum of properties when given the option to view at an open house, perhaps falling in love with a property that they would not have expected would fit their needs. We can all remember the television programs where the buyers were blown away with the ‘wildcard’ property.

22 Garnie Avenue, Erskine – Saturday and Sunday from 12 to 2pm

14 Park Green, Erskine – Saturday from 12 to 2pm

7 Park Glade, Erskine – Saturday and Sunday from 12 – 2pm

47 Sunnylaw Drive, Paisley – Saturday and Sunday from 12 to 2pm

5A Viking Way, Renfrew – Saturday and Sunday from 12 – 2pm

44 Moorpark Square, Renfrew – Saturday and Sunday from 12 – 2pm

142 Moorpark Square, Renfrew for both Sat and Sun 12 – 2pm

Contact Us

For more information, please call 0141 886 5678

A great year for our Estate Agency and the local property market!

While there have been challenges for both buyers and sellers this year, the property market in Renfrewshire has experienced considerable improvements and we are delighted to announce that our Estate Agency has secured over £20 million worth of property sales on behalf of our clients, in 2016.

The volume of residential sales in Renfrewshire increased in 2016. The latest Registers of Scotland house price report shows a 19% increase in quarter 2 sales this financial year in the local area, compared to quarter 2 last year. For the same period, the average property value in Renfrewshire increased by 3%. Clearly despite uncertainty surrounding Brexit and more recently the US presidential election, the local market has shown resilience.

In 2016, we have not only seen more buyers in the local market, but also more sales being agreed and in shorter periods of times, with Walker Laird selling over 100 properties in Renfrew alone. This year has also brought more favourable conditions for sellers, with growing demand and a steady supply of new properties. In 2016 we witnessed the frequent return of closing dates – an impressive 44 times at Walker Laird this year.

Competition amongst buyers has been particularly obvious when marketing family houses, as we found that some buyers were prepared to pay a premium price for the right property. One property for example, went to a closing date with 12 offers in place, the highest of which was 28% above asking price.

The demand for good family size accommodation looks set to continue, so if you want to know how much your home is worth in today’s market or get advice about moving in 2017, we would be delighted to provide you with an up to date and free valuation. Buyers trying to identify their ideal home should also get in touch and speak to us about using our matching service.

We can offer competitive fee structures for sellers coming to the market early in the new year, which is the ideal time to take advantage of that early rush and pick up of activity after Christmas. We can also offer a full deferral of the up-front costs.

Get In Touch

Call 886 5678 and speak to one of our experienced team.